Our PureSegmentation™ research confirms that price works in relationship with brand value, and is rarely the only reason someone buys.

No one questions that pricing plays a role in supplement sales. The real question is how much it actually influences behavior — and what other factors have more power over the decision to buy, switch, or stay loyal. What about the mother of two who stayed loyal to a B complex that cost twice as much as other reputable options? What would make her switch?

There are private-label and mass-market brands that compete primarily on price. Shoppers on Amazon can filter for cost per count or chase “Prime Big Deals.” There are also premium and practitioner brands that use price as a signal of quality or scientific rigor — and deploy discounts or rewards to stimulate trial and repeat purchase. In all cases, price is always working in relationship with brand value. It may be a powerful driver, but it is rarely the only reason someone buys.

When we developed our proprietary, census-balanced Supplement Consumer PureSegmentation™ Research, we already knew from prior work that while price mattered, it was rarely the decisive factor in supplement purchasing.

So we set out to test that assumption — placing pricing within the broader context of supplement behavior, brand switching, trial motivation, and engagement. What we found was a far more intricate web of forces that shaped both first-time and repeat purchase decisions.

The role of pricing in supplement behavior

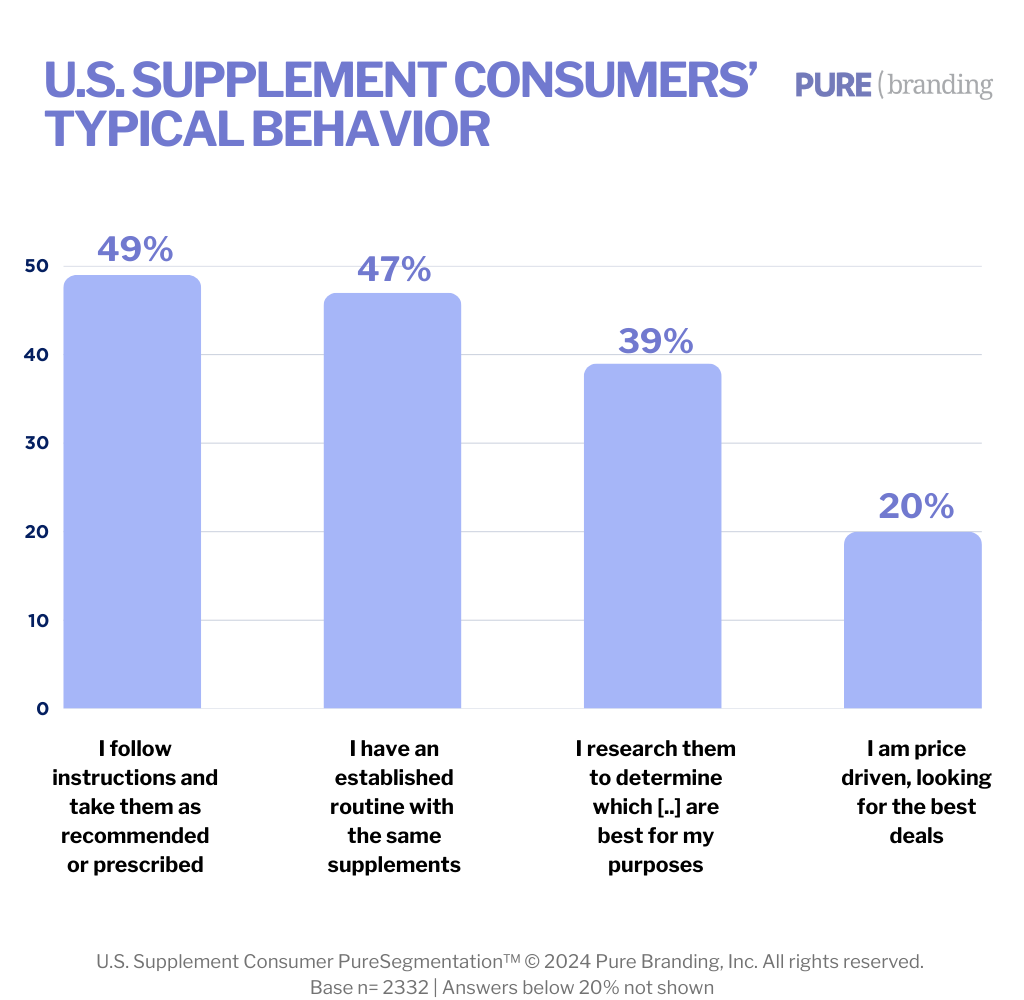

We asked consumers to describe how they typically interacted with supplements — whether they experimented, researched, followed instructions, stuck to an established routine, took them when they remembered or felt the need, or sought the best deal.

Overall, being price-driven and looking for the best deal ranked fourth, selected by 20 percent of supplement users. Far more important were following instructions and taking them as recommended (49 percent), having an established routine with the same supplement brands (47 percent), and researching which supplements were best for them (39 percent).

The segment that valued research the most under-indexed for being price-driven. The segment that was the least research-oriented or routine-driven— an irregular and spontaneous group that was most likely to take supplements when they remembered or felt the need—was the most likely to be price-driven and looking for the best deals. On the surface, this suggested that those who researched brands were less price-driven than those who did not.

When we looked at the segment that was most likely to both follow instructions (77 percent) and have an established routine (65 percent), that segment over-indexed for being price-driven.

Next, we analyzed the impact of pricing in relation to switching behavior.

Switching behavior

We asked consumers how often they switched brands of supplements and, when they did, what typically prompted that change.

Across the total sample, about 61 percent of supplement users said they either never or rarely switched brands. 37 percent said they often or sometimes switched.

Among all possible reasons for switching, better pricing or being on sale led at 39 percent, followed closely by wanting to try something new (37 percent) and doctor or practitioner recommendation (29 percent). Friends and family recommendations were next (27 percent), followed by dissatisfaction with the current brand (24 percent).

The segment that placed the greatest importance on research was the second most likely segment to switch (53 percent). Their top reason for switching was wanting to try something new, followed by better pricing and dissatisfaction with their current brand.

At the opposite end, the irregular and spontaneous segment—those who tended to take supplements when they remembered or felt the need—also over-indexed for switching. Their top reasons were wanting to try something new, followed by better pricing.

Meanwhile, the segment that over-indexed for following instructions and having an established routine were the least likely to switch. The were most influenced by price and doctor recommendation.

It was clear from the data that price could influence switching behavior, which is why it remains critical for brands to pay attention to pricing strategy. But it was far from the whole story. Just as important was how a brand engaged with its customers to keep them from switching—keeping things fresh so they didn’t seek novelty elsewhere, focusing on satisfaction, and building credibility among professional communities.

Switching from is the first step. Switching to is the more important next step.

Motivating first-time purchase

We asked consumers what would most likely push them closer to buying a supplement they hadn’t purchased before.

Across the total sample, the leading motivator was strong verified customer reviews (45 percent), followed by a promotional offer (20 percent off) at 35 percent, a clinical paper demonstrating efficacy (21 percent), and an impressive scientific or medical advisory board (22 percent). Taken together, the data showed that consumers balanced credibility and incentive—proof and price both played roles, but not equal ones.

The segment that placed the highest importance on research valued verified customer reviews the most (56 percent). While a promotional offer of 20 percent off was second (33 percent), this segment over-indexed for clinical papers and impressive advisory boards—demonstrating that almost as important as price in driving trial were trust and transparency.

By contrast, the price-sensitive, routine-driven segment was far more responsive to promotional offers and less moved by customer reviews or scientific evidence.

As expected, the irregular and spontaneous segment responded strongly to promotional pricing. For them, discounts and deals were a practical cue to act.

Overall, the data made clear that price could nudge first-time purchase, but credibility closed it. Brands that depended too heavily on promotions risked attracting trial without trust—while those that combined transparent proof with fair value could convert first-time buyers into long-term customers.

Retention and building loyalty

We asked consumers to imagine they had a favorite supplement brand they’d taken daily for the past year, and then tell us what kind of communication or benefits they would most like to receive from that brand.

Across the total sample, the top responses were trustworthy information and nutritional or lifestyle education (34 percent) and access to a rewards or loyalty program (34 percent). Close behind were notifications of upcoming sales and promotions (29 percent), recommendations of other products that might help (26 percent), and access to at-home tools or testing (22 percent). In short, ongoing engagement was about connection and content at least as much as it was about discounts and deals.

The research-oriented segment over-indexed for trustworthy information and education (42 percent). Rewards programs ranked second, followed by recommendations to help accomplish health goals. For this group, loyalty came from learning, achieving outcomes, and being recognized for their efforts.

The price-sensitive, routine-driven segment showed the opposite pattern, over-indexing for notifications of upcoming sales and access to rewards programs. For them, retention had a transactional dimension.

Finally, the irregular and spontaneous segment showed no single dominant preference, spreading interest across promotions, rewards, and recommendations.

Overall, the data underscored that developing a relationship with customers was a two-way street: those who wanted educational engagement also wanted recognition for their interest, and those who watched their dollars wanted the brand to watch its pricing.

But price increases are a part of brand life. What then? Or the better question may be: what should a brand invest in so customers recognize the value behind that investment?

Transparency and the willingness to pay more

We asked consumers to what extent they agreed with the statement: “I would pay more for a transparent herbal and/or dietary supplement company.”

Across the total sample, 70 percent agreed or strongly agreed that transparency was worth paying for. Of that, 27 percent strongly agreed and 43 percent agreed, while 20 percent were neutral and 9 percent disagreed. The strongly agreed group represented those most likely to act on this belief in real life, while those who agreed expressed aspiration more than certainty.

The research-oriented segment—the one most motivated by credible information and third-party validation—was also among the most willing to pay more for transparency, with 33 percent strongly agreeing. For them, transparency equaled proof, and proof justified premium.

The price-sensitive, routine-driven segment told a different story. They under-indexed in willingness to pay more for transparency. It mattered to them, but not enough to warrant a higher cost.

The irregular and spontaneous segment—open to experimentation and motivated by discovery—also under-indexed, but for different reasons. They valued freshness, innovation, and experience over transparency; it was not that they rejected honesty, but that other attributes carried more weight.

Overall, the data made one thing clear: transparency was a premium signal, but its value depended on what each segment saw in it.

For some, it validated science and integrity. For others, it was simply table stakes.

In the end, transparency didn’t just justify higher pricing—it could be the factor that sustained loyalty when prices inevitably rose.

The PureSegment’s journey in relation to price

Pricing is a part of every customer’s journey with a supplement brand. The PureSegmentation data show that pricing ranked high as an influence when viewed in total numbers. But when seen through the lens of segmentation, it became clear that price played a very different role for different consumers.

The research-oriented segment was the most inquisitive of all supplement consumers. Nearly half described having an established routine, but unlike other routine-driven groups, they were also the most likely to say they “researched which supplements are best.”

One truth stands out: price and brand work hand in hand for the first purchase, but brand does the heavy lifting for every decision that follows.

This curiosity showed up in their behavior: they switched brands more often than most, usually to “try something new” first, with “better pricing” and “dissatisfaction” following at a distance.

When considering a new supplement, promotional offers barely registered—what moved them were verified reviews and credible validation. Once loyal, they wanted trustworthy information and education that deepened their understanding of what they were taking.

For this segment, pricing wasn’t an incentive; it was a data point. Knowledge, not cost, guided their brand journey.

The routine-driven segment represented a more structured mindset. They were among the most likely to say they “followed instructions and took supplements as recommended,” and they showed one of the highest levels of routine. But within that discipline lay a clear price sensitivity.

When they switched, price played a central role—often alongside doctor recommendations or dissatisfaction. Promotional offers had real influence for them at the first-purchase stage, while reviews and scientific evidence mattered less.

Once loyal, they wanted to feel recognized through rewards programs or notified about upcoming sales. For this segment, price was part of a system of order and validation—it didn’t drive impulsivity, but it reassured them that they were making a smart, sanctioned choice.

The irregular and spontaneous segment was the least routine-oriented and the most open to experimentation. They took supplements “when they felt a need,” and switching was part of their normal rhythm.

They changed brands primarily to “try something new,” more than for price or dissatisfaction. While better pricing influenced some of their decisions, novelty remained the stronger motivator.

At the first-purchase stage, they were the most responsive to promotional offers—discounts served as an easy, low-risk entry point. But their loyalty was short-lived. They were less engaged by education, loyalty programs, or transparency claims, showing little sustained interest once the initial novelty faded.

For this segment, price acted as an invitation, not a commitment. They valued variety, immediacy, and discovery over brand depth or long-term trust.

Viewed together, these segment journeys showed that price didn’t drive the same kind of relationship for every customer.

For one, it informed choice but never defined it. For another, it was a measure of fairness and discipline. And for a third, it was a short-term motivator—an easy reason to start, and an easier reason to leave.

Across all three, one truth stood out: price and brand work hand in hand for the first purchase, but brand does the heavy lifting for every decision that follows.

This article is part of our ongoing PureSegmentation™ Insights series, where we share new findings and perspectives from our proprietary supplement consumer research.